Bitcoin might commerce across the clock, however its liquidity is now not the case. The asset, which was presupposed to be extra resilient after absorbing billions of {dollars} in institutional capital by ETFs, has as a substitute fashioned a twin persona, showing deep and orderly throughout New York buying and selling hours however turning into significantly extra fragile when the desks of Wall Avenue go darkish.

Kaiko’s newest knowledge launched this week quantifies what many merchants have been feeling for a while. In different phrases, the identical ETF-driven maturation that deepened Bitcoin’s weekday market is hollowing out weekend buying and selling, making a two-tier buying and selling atmosphere the place smaller individuals soak up a disproportionate share of the danger.

Based on Kaidaka’s evaluation, because the Spot Bitcoin ETF was launched in January 2024, institutional investor participation has been concentrated throughout U.S. weekday buying and selling hours, and their share of buying and selling quantity throughout these hours has risen to about 47%.

At present, weekday buying and selling volumes are persistently twice that of weekends, and the hole widened all through 2025 and into 2026 as institutional allocations elevated. The promise of a 24/7 unified market, which was presupposed to be the function that distinguishes cryptocurrencies from every little thing else within the monetary world, is definitely weakening. As a result of whereas Bitcoin continues to be open each Saturday and Sunday, the capital that gives that depth just isn’t.

BTC nonetheless trades 24/7, however critical liquidity is turning into extra selective

This alteration is seen in what merchants discuss with as order guide depth, or the whole quantity of purchase and promote orders which might be inside a sure vary of the present worth. This is a vital measure of liquidity and serves as a tough measure of how a lot purchase or promote the market can soak up earlier than the worth begins to maneuver in opposition to you.

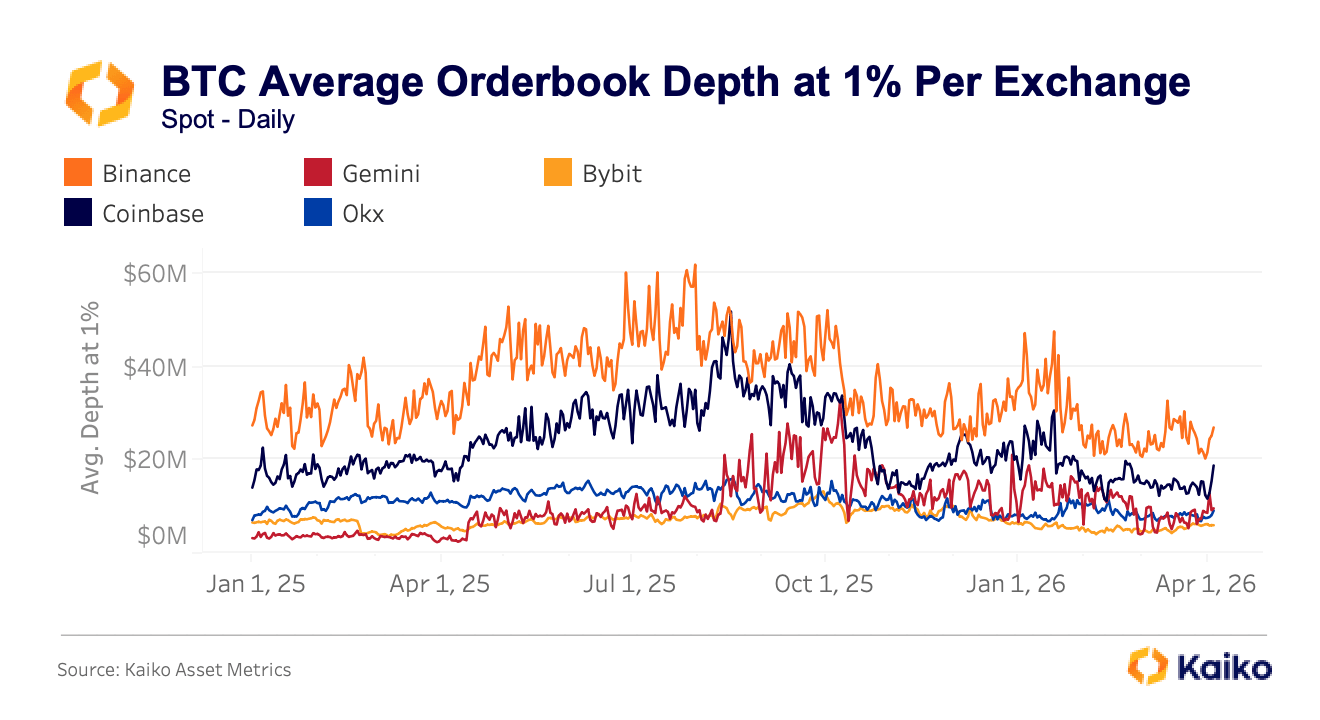

Kaiko tracks 1% depth from the midway level. This implies all remaining orders inside 1% above or beneath the present Bitcoin worth. This quantity varies vastly relying on the place you commerce. Binance persistently affords a depth of round $30 million at that stage, whereas Coinbase ranges from $16 million to $20 million.

Buying and selling volumes on secondary exchanges similar to Gemini, Bybit, and OKX are sometimes $10 million to $15 million, making a 2x to 3x distinction and instantly main to cost deterioration for many who meaningfully place orders on the improper platform.

This distinction just isn’t secure underneath stress and actually tends to blow out virtually precisely at the most expensive instances. Throughout the tariff-driven sell-off final October, Bitcoin spot costs diverged considerably between venues inside minutes, with Binance lagging at $102,318, OKX at $102,142, and Bybit at $101,675, with the $643 unfold lasting for minutes slightly than seconds as could be anticipated if regular automated arbitrage mechanisms had been successfully closing the hole.

This sample was repeated throughout geopolitical escalation within the Center East in March 2026, when BTC-USDT buying and selling prices on Bybit spiked 230% from regular ranges, and comparable spikes occurred on OKX and Binance. Each episodes started over the weekend, when institutional individuals had already exited and orders had been at their thinnest.

When Wall Avenue closes, the distinction between ‘worth’ and yours can widen quickly

This has very actual and concrete penalties. Bitcoin worth fell beneath $78,000 on Saturday afternoon, February 1st, and inside 24 hours, greater than 335,000 merchants had liquidated roughly $2.2 billion.

This drawdown was not as a consequence of a basic collapse particular to cryptocurrencies, however slightly was amplified by structurally illiquidity over the weekend. Because of this the market just isn’t reacting to unhealthy information about Bitcoin, however slightly to the mechanical actuality that there are fewer individuals to soak up promoting strain.

A subsequent Van Eck evaluation, which extensively analyzed February’s crash, discovered that Bitcoin’s one-day worth motion on February 5 ranked as one of many asset’s quickest on document, measured by statistical measures of pace and measurement. Stochastic fashions predict such excessive occasions to be uncommon, however they’ve now surfaced twice in 5 months.

Merchants who purchase and promote on secondary venues on Saturday nights or in periods of heightened volatility might not obtain costs near the consensus Bitcoin worth they consider they’re buying and selling.

The hole between quoted and executed costs tends to widen when the consequences of unhealthy executions are most extreme, and the asymmetry is most extreme for individuals who lack the institutional infrastructure to attend for higher phrases.

It’s clear that retail merchants are nonetheless taking part in cryptocurrencies, however Kaiko’s analysis means that they’re being relegated to thinner, much less protected components of cryptocurrencies. From a time perspective, retail commerce is extra dangerous throughout after-hours, weekends, and intervals when ETF flows are low and institutional market-making recedes.

Geographically, retail nonetheless dominates the market, which bears no resemblance to US ETF-driven Bitcoin buying and selling, with South Korea persevering with to rely closely on retail participation and altcoin buying and selling volumes, whereas Turkish crypto exercise displays macro stress hedging and stablecoin demand slightly than the surge in institutional exercise within the US.

There may be additionally an asset side to the break up.

Institutional capital, channeled by ETFs and prime brokerage preparations, has standardized Bitcoin buying and selling above all different cryptocurrencies, concentrating refined market making and deep liquidity in BTC, leaving the remainder of the area (altcoins, native foreign money pairs, small platforms) with skinny protection and fewer skilled help. Speculative and fragmented exercise persists in abundance throughout a broader vary of markets, slightly than in the identical exchanges or time zones during which monetary establishments are established.

Market high quality differs even for a similar Bitcoin

What emerges from this knowledge is turning into more and more tough to disclaim. Two Bitcoin markets might now be working in parallel. A deeper, extra environment friendly, institutional-style weekday market, accessible by ETFs and main venues, and a thinner, extra risky after-hours market, the place smaller merchants are prone to be current and who usually tend to bear the prices of poor execution.

In concept, Bitcoin is identical asset for everybody, however in actuality, the standard of the market you encounter relies upon largely on when and the place you commerce.

None of that is an argument that ETFs destroyed Bitcoin. Institutional investor participation has introduced actual advantages, together with deepening mixture liquidity, decrease common spreads in regular instances, and a level of legitimacy that didn’t exist in earlier cycles.

Cumulative web inflows into U.S. Spot Bitcoin ETFs have remained at round $53 billion to $54 billion since their inception, even after massive outflows in early 2026, permitting them to soak up massive quantities of capital and survive true volatility with out collapsing.

However the identical forces that improved Bitcoin’s greatest instances seem to have revealed how uneven the market turns into when individuals retreat, bringing maturity to some periods whereas leaving others weak.