Simply as Bitcoin enters one of many yr’s most essential macro exams, the previous “Promote in Might” warning is shedding its validity.

Whereas US shares have endured repeatedly from Might to October, Bitcoin’s subsequent transfer will depend upon whether or not inflation, employment, and Fed indicators maintain threat urge for food.

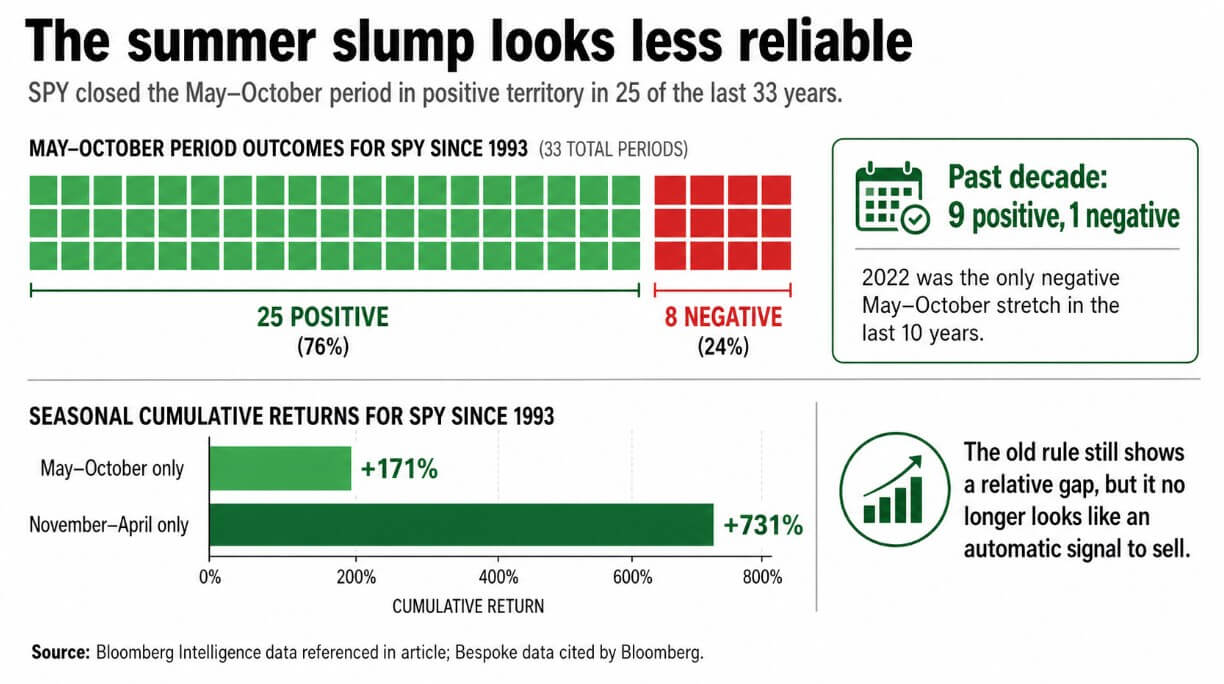

The S&P 500 ETF has completed in constructive territory from Might via October in 25 of the previous 33 years, and has had only one unfavourable summer season interval over the previous 10 years, in accordance with knowledge from Bloomberg Intelligence.

In keeping with customized knowledge cited by Bloomberg, the cumulative return for proudly owning SPY because the ETF’s debut in 1993 has been about 171% from Might to October alone. It is a substantial quantity and is simply considerably lower than the 731% I earned on my prolonged keep from November to April alone.

Regardless of seasonal variations in efficiency, the cliché that Might routinely means a promote does not maintain true.

Guidelines which will not work

The logic behind this previous adage is that company earnings are weak, buying and selling desks are stretched skinny, and traders flip to money or bonds till the autumn.

This technique has labored properly for many years and was constructed for a market the place institutional cash strikes slowly and threat urge for food follows a predictable rhythm.

Bitcoin has spent two years plumbing conventional portfolio flows straight. In keeping with knowledge from Pharcyde Buyers, the US Bitcoin Spot ETF acquired roughly $1.5 billion in inflows from April 17 to April 24, bringing cumulative web inflows to roughly $58.3 billion.

This market construction places Bitcoin into the identical threat urge for food mechanisms that drive shares, giving it direct publicity to issues that make institutional traders wish to personal it.

If institutional capital doesn’t reflexively keep away from threat heading into the summer season, BTC may keep away from one of many psychological headwinds that traditionally hit speculative belongings in Might.

The Fed’s personal analysis exhibits that the bid-ask spreads of crypto ETPs are roughly equal to the spreads of equally sized fairness ETFs and ETPs, arguing that the NAV premium of crypto funds needs to be monitored as a measure of how interconnected crypto and fairness markets are.

Bitcoin Might Settings

Whether or not Bitcoin has a summer season with fewer headwinds will rely nearly fully on what the following six weeks of knowledge deliver.

Coverage choices had been made on the Fed assembly held from April Twenty eighth to Twenty ninth, and on April Twenty ninth, Fed Chairman Jerome Powell held a press convention. The Bureau of Financial Evaluation will launch first quarter GDP and March PCE on April thirtieth.

The April employment report will likely be launched on Might eighth, the April CPI will likely be launched on Might twelfth, the FOMC minutes from the April assembly will likely be launched on Might twentieth, and the following full Fed assembly will likely be held on June Sixteenth-Seventeenth.

| date | occasion | Newest studying/setup in article | Why does the market care? | BTC learn via |

|---|---|---|---|---|

| April Twenty eighth-Twenty ninth | Fed assembly + Powell press convention | Fed will stay stalled except knowledge forces a shift | Rates of interest, liquidity, and the way laborious the Fed pushes again on charge lower expectations set the tone | Affected person and data-dependent Fed helps threat urge for food and helps Bitcoin keep away from seasonal threat aversion narrative |

| April thirtieth | Q1 GDP + March PCE | GDPNow estimates first-quarter progress at 1.2% as of April twenty first. PCE for February was 2.8% and core PCE was 3.0%. | Reveals whether or not progress is slowing cleanly or sliding towards stagflation, and whether or not inflation has cooled sufficient to maintain expectations of easing. | Average however secure progress with subdued inflation is constructive for BTC. Slowing financial progress and persistently excessive inflation are issues |

| Might eighth | April payroll calculation | Labor market remained sturdy sufficient in March to make Fed cautious | If the employment state of affairs improves, expectations for rate of interest cuts may be maintained. Scorching printing might enhance yields | Cooling labor knowledge with out concern of recession is bullish for BTC. Reacceleration of hiring may weigh on BTC via rising yields |

| Might twelfth | April shopper worth index | March CPI was 3.3% year-on-year, and core CPI was 2.6%. The April CPI nowcast launched by the Cleveland Fed was 3.56% yr over yr. | CPI is the cleanest short-term take a look at to find out whether or not inflation is accelerating once more | Softer printing helps within the risk-on case for BTC. Excessive-profile print publications can revive “Might Cell” via tight monetary circumstances |

| Might twentieth | FOMC Minutes | Markets need particulars on how involved officers had been about inflation and rate of interest cuts | Minutes can both strengthen or soften the message of Powell’s press convention | BTC may commerce like a high-beta macro asset if minutes point out a excessive bar for charge cuts |

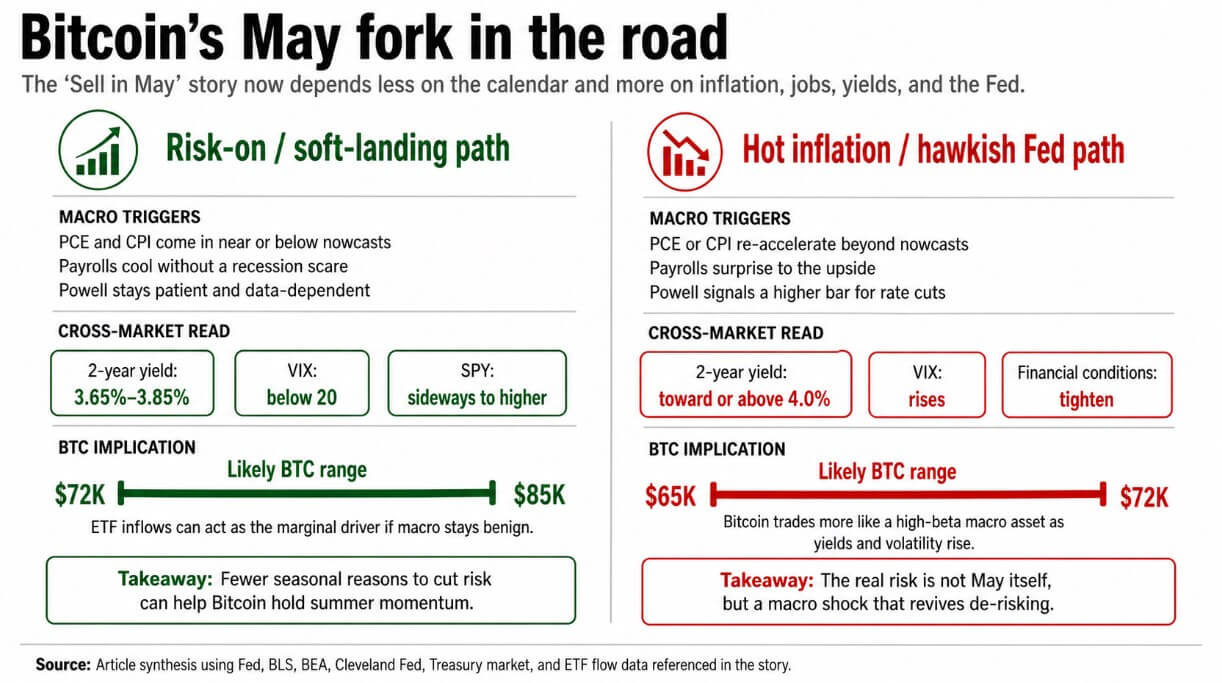

| June Sixteenth-Seventeenth | Subsequent Fed Normal Assembly | By then, the market can have GDP, PCE, salaries, CPI, and April minutes launched. | That is the purpose the place the Might knowledge run will affirm or break the summer season risk-on idea. | If the macros stay favorable, BTC can preserve a variety between $72,000 and $85,000 inside this window. If inflation and yields rise, the draw back to $65,000-$72,000 turns into extra lifelike. |

This sequence of occasions both confirms that “Promote in Might” has misplaced its macro foundation, or this time it will likely be rebuilt.

The Atlanta Fed’s GDPNow, as of April 21, places the expansion charge within the first quarter at 1.2%, whereas the official GDP for the fourth quarter of 2025 is 0.7%.

The CPI in March was 3.3% year-on-year, the core CPI was 2.6%, and the vitality index rose 10.9% month-on-month. PCE in February was 2.8% and core PCE was 3.0%.

In keeping with the Cleveland Fed’s nowcast as of April 28, April CPI was 3.56% year-on-year, and April PCE was 3.60%. The March Fed SEP raised each median 2026 PCE and core PCE to 2.7%, with 17 out of 19 members marking inflation dangers as skewed to the upside.

As of late April, the cross-market state of affairs was below management. The two-year authorities bond yield was 3.78%, the 10-year authorities bond yield was 4.31%, the VIX was 18.02, and BTC was within the $76,000 zone.

BlackRock’s Spring Outlook frames the present settings as a trade-off for benign stagflation, with the Fed remaining on pause and transferring to gradual easing provided that inflation continues to sluggish or progress stays average.

If April PCE and Might CPI stay near or weaker than present nowcasts, and April payrolls cool with out triggering recession considerations, the Fed may actually proceed counting on the information.

This is able to lock the two-year bond yield into a variety of roughly 3.65% to three.85%, hold the VIX beneath 20, and hold the SPY flat to excessive. On this context, ETF inflows would be the marginal driver for Bitcoin.

Institutional allocators who’ve constructed Bitcoin positions via IBIT or peer funds haven’t any clear seasonal motive to scale back their publicity.

Bitcoin may stay within the $72,000 to $85,000 vary till the June Fed window. If core inflation seems to be softer than feared, whereas the expansion knowledge stays unconcerned and the employment knowledge is properly underperformed, markets may re-price in a clearer easing path for the second half of 2025.

The markets wherein SPY was constructive in 25 of the 33 intervals from Might to October are markets the place the idea for motion to scale back threat in the summertime is weakening yr by yr.

Inflation brings again “sell-in-may”

Treasury yields will rise if PCE and CPI reaccelerate above their nowcasts, if April payrolls present sudden upside, or if Chairman Powell makes it clear in his April 29 press convention that the hurdles for cuts are increased than the market expects.

If the two-year bond yield rises above 4%, monetary circumstances will tighten, fairness multiples will likely be compressed, and the liquidity background that supported Bitcoin’s rise within the ETF period will disappear.

In that atmosphere, BTC trades as a high-beta macro asset. A pullback to the $65,000 to $72,000 vary is probably going, pushed down by the identical threat urge for food that has been pushing it increased.

In keeping with the Philadelphia Fed’s Concern Index, the primary quarter survey confirmed that the likelihood of GDP decline within the second quarter was 20.9%, a stage excessive sufficient to maintain recession threat as a tail threat.

If GDP declines unexpectedly whereas inflation stays low, the Fed will likely be caught in traditional stagflation, the place neither charge cuts nor charge hikes can remedy the issue. That stagflation bind is definitely the biting model.

Bitcoin absorbed Wall Avenue’s infrastructure and inherited its constraints together with its capital. Seasonal lore has all the time represented the concept that summer season is a time when macro imbalances are priced in, liquidity thins, and traders rethink what they wish to personal.

The following six weeks will take a look at whether or not the macro regime that drove Bitcoin to all-time highs can face up to inflation knowledge.

The following take a look at is a direct one. If inflation subsides and yields stay subdued, Bitcoin might proceed to deal with Might as a macro checkpoint somewhat than a promote sign. If the CPI, PCE, or jobs report forces the Fed to return to a extra aggressive stance, seasonal warnings will return via tightening monetary circumstances and BTC’s ETF-era help will likely be examined via the June assembly.