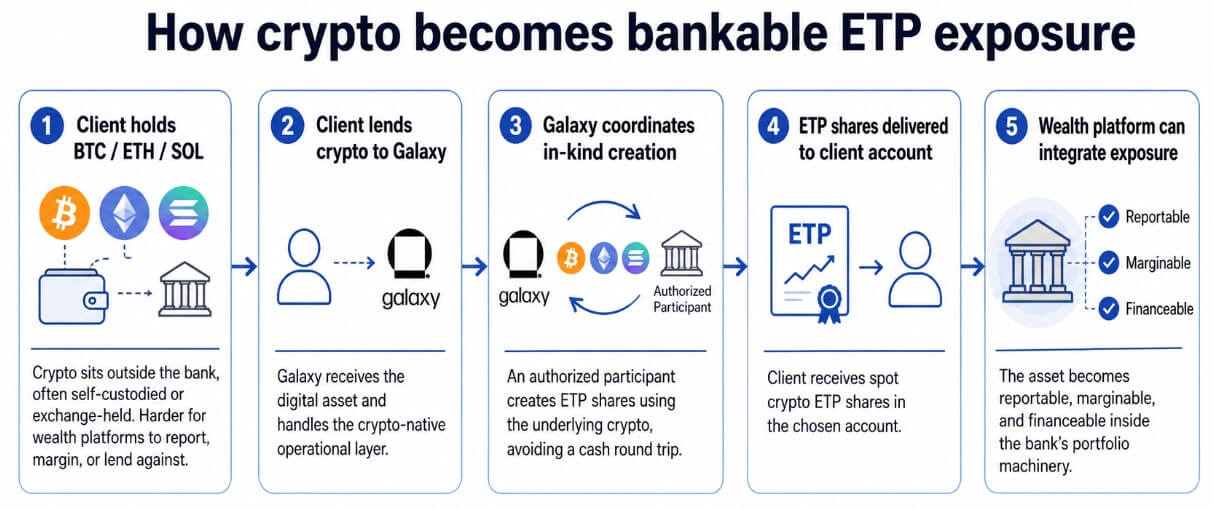

Morgan Stanley introduced on June 5 that eligible wealth administration shoppers can now lend Bitcoin, Ethereum or Solana to Galaxy Digital and obtain shares of spot crypto exchange-traded merchandise in return.

Galaxy will coordinate bodily creation with permitted members and ship ETP shares on to the shopper’s chosen account. Onboarding timelines that beforehand exceeded 4 weeks might be decreased by as much as 75%.

For purchasers referred by Morgan Stanley, Galaxy has lowered the minimal deal quantity from $25 million to $5 million.

The U.S.-traded Spot Bitcoin ETF posted a historic $4.4 billion in web outflows for 13 consecutive weeks ending in early June. Bitcoin has fallen about 53% from its October 2025 excessive of round $126,200, reaching $60,000 at one level this week.

Towards this backdrop, Morgan Stanley’s deal supplies high-net-worth shoppers with direct holdings of cash which can be built-in into the financial institution’s portfolio construction, marginable, reportable, and have entry to the identical infrastructure that already helps securities lending, margin accounts, and personal banking.

The regulatory layer that made this attainable

In July 2025, the SEC permitted the in-kind creation and redemption of crypto ETPs, eradicating a central structural impediment.

This variation permits approved members to create and redeem Spot Crypto ETP shares utilizing the underlying crypto property, making it work nearer to how commodity ETPs already work.

Galaxy can now take prospects’ BTC, use it to create bodily ETP shares, and ship these shares with out making a taxable sale of the underlying property. Underneath the earlier guidelines, this workflow required round-trip money conversion.

Morgan Stanley has restricted its position to introductions and buyer training, whereas Galaxy oversees onboarding and has publicity to cryptocurrency operations.

This division will enable Morgan Stanley to stay on the regulated securities aspect of the transaction whereas Galaxy will take operational threat into cryptocurrencies.

Exterior crypto property, beforehand held in self-custody or on exchanges, might be moved into bankable portfolios, function margin collateral, and combine with reporting and lending providers.

Three fashions for 3 theories

Morgan Stanley’s association falls inside broader institutional variations over what types of crypto publicity banks can safely acknowledge, with three fashions at present working in parallel.

The primary is ETP collateral, which is essentially the most bank-friendly kind as a result of banks perceive how one can value, retailer, margin, and liquidate registered securities. JPMorgan moved right here first, accepting BlackRock’s IBIT inventory as collateral for a mortgage earlier than increasing additional.

Morgan Stanley and Galaxy’s settlement extends this mannequin by changing cryptocurrencies held exterior banks into ETP shares, which shall be built-in into current asset administration, margin and lending workflows.

The second mannequin is direct crypto collateral and represents a bigger structural leap. JPMorgan had deliberate to permit institutional shoppers to immediately pledge BTC and ETH towards loans by the top of 2025, with collateral property held by third-party custodians. The financial institution has not publicly confirmed which merchandise are literally in operation, and the state of affairs stays based mostly on reported plans.

| mannequin | banking consolation stage | Foremost asset varieties | Instance from article | What banks like | Foremost dangers |

|---|---|---|---|---|---|

| ETP collateral | costly | Spot Bitcoin/Digital Foreign money ETP Share | Morgan Stanley/Galaxy; JP Morgan accepts IBIT collateral | Acquainted securities wrappers, custody, pricing, and margins | ETF outflows propagate promoting by institutional buyers |

| Direct cryptocurrency collateral | medium to low | Straight collateralize BTC/ETH | Report on JP Morgan’s BTC/ETH Collateral Plan | Extra direct use of cryptocurrencies as stability sheet collateral | Volatility, custody, margin calls, liquidation rights |

| Tokenized Collateral Various | rising | Tokenized authorities bonds, MMFs, and deposits | Customary Chartered/OKX/BlackRock BUIDL; HSBC Tokenized Deposit | Collateral leg with excessive yield and low volatility | Fee, authorized and platform interoperability dangers |

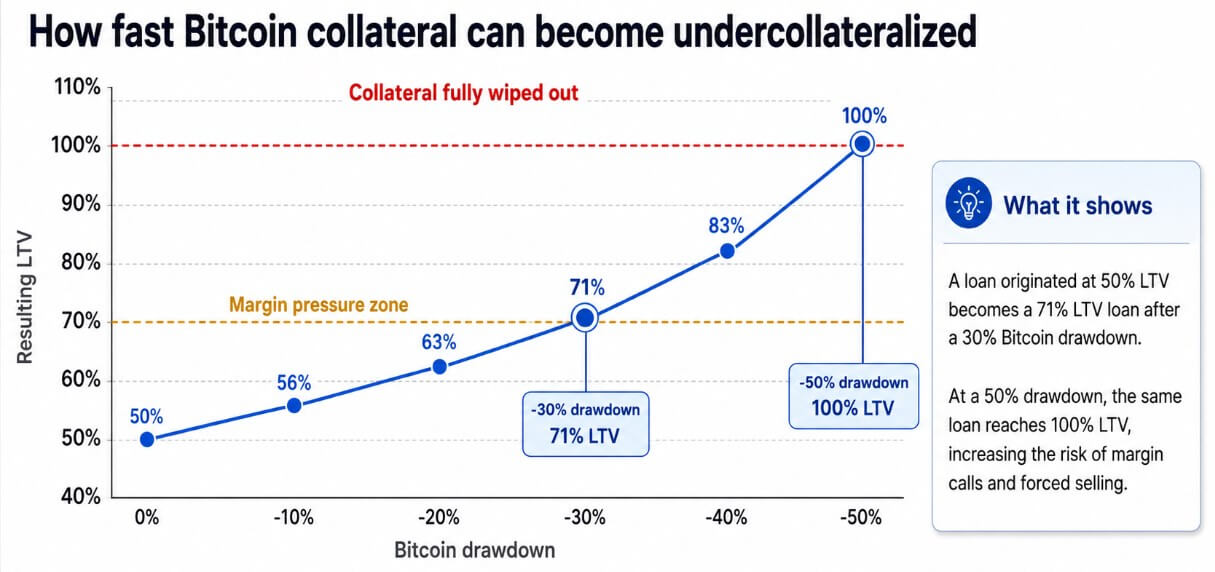

As soon as operational, banks will deal with BTC and ETH in the identical method they already deal with listed shares in margin accounts, with real-time valuations, haircuts, and computerized margin calls.

A mortgage that begins at 50% loan-to-value turns into a 71% LTV mortgage after a 30% Bitcoin drawdown. A 50% drawdown would take the identical mortgage to 100%, fully erasing the collateral.

The $1.8 billion in compelled crypto liquidations recorded on June 3 alone is the most important single-day determine since February 2026 and exhibits what leverage can create in high-velocity markets.

The third mannequin, tokenized collateral substitution, might show to be essentially the most sturdy. Whereas banks choose tokenized US Treasuries and cash market funds as collateral, cryptocurrencies stay as traded threat property.

On April 28, OKX, BlackRock and Customary Chartered launched a framework that enables institutional buyers to pledge BlackRock’s BUIDL tokenized Treasury funds as yield-bearing margin collateral to OKX, with Customary Chartered performing as the primary G-SIB custodian in such an association.

Prospects can earn yield on the collateral they’d in any other case have idled, and Customary Chartered handles regulated off-exchange custody, preserving property separate from the change’s personal holdings.

What banks are literally constructing

Customary Chartered’s off-exchange mannequin with OKX implies that crypto-native buying and selling venues would require a regulated G-SIB wrapper to draw essentially the most cautious institutional buyers.

BNY is constructing a digital asset platform that mixes custody, collateral administration, lending, funds, and 24/7 liquidity rails, positioning it because the infrastructure basis upon which crypto lending and tokenized asset markets will function.

Citi frames its position round funds, storage of stablecoin reserves, and crypto ETF custody providers, and claims its position is plumbing.

All main banks are competing to manage the wrapper, custodian, collateral agent, or service infrastructure round which Bitcoin circulates.

Two paths by means of the identical pipe

In a bullish case, regulatory readability and stronger custody controls will normalize the usage of BTC and ETH as collateral for institutional buyers.

In line with Citi’s June 2026 Tokenization Report, world tokenized property are at present round $17 billion, with a bull case forecast of $8.2 trillion in 2030.

If this trajectory holds, crypto collateral will grow to be a routine characteristic of financial institution lending, tokenized US Treasuries will develop as the popular institutional margin asset, and Bitcoin will grow to be much more helpful as a stability sheet automobile.

The pipeline that Morgan Stanley and Galaxy are assembling shall be expanded at scale throughout personal banking, bringing self-custodial property into managed portfolios the place they are often funded, reported and deployed.

Within the bearish case, volatility and operational threat will hold banks locked into the ETP wrapper. Direct Bitcoin collateral packages stay slender in scope, have excessive haircuts, and have restricted attain past a slender organizational base.

Banks depend on tokenized U.S. Treasuries and deposits, and whereas HSBC will develop tokenized deposit providers to U.S. prospects in April 2026, enabling 24/7 on-chain funds motion with out public chain settlement threat, uncooked BTC lending stays restricted to a small variety of crypto-native lenders and hedge funds.

Bitcoin ETF outflows have grow to be a recurring phenomenon as regulated wrappers appeal to capital and it flows out the identical door when sentiment modifications.

leverage loop

Neither situation eliminates the structural influence of the collateral itself.

Galaxy Analysis estimated that crypto-backed lending will attain $73.59 billion in Q3 2025, break up between DeFi lending (55.7%), CeFi (33.1%), and crypto-backed stablecoins (11.2%).

As banks develop from ETP collateral to direct BTC and ETH lending, Bitcoin value actions will more and more mirror institutional deleveraging cycles.

The $4.4 billion spot ETF outflow that pushed Bitcoin under $60,000 this week exhibits how shortly regulated wrappers can propagate institutional promoting. Including margin calls on crypto-backed loans on to that mechanism would end in extra drawdowns forcing promoting than the market has been in a position to deal with to this point.

Morgan Stanley’s cope with Galaxy is an asset administration funnel. Exterior crypto property enter banks’ portfolio constructions, changing into loanable and reportable, rising correlation to something that causes institutional buyers to scale back threat.

Bitcoin adoption shall be built-in into the identical collateral loop that governs all different asset lessons, with all of the structural appreciation and deleveraging publicity that comes with it.