Bitcoin’s extended decline has pressured crypto firms to chop workers, automate extra work, and abandon enlargement plans that characterised the final bull market. On the similar time, it has additionally created probably the most takeover intervals within the {industry}.

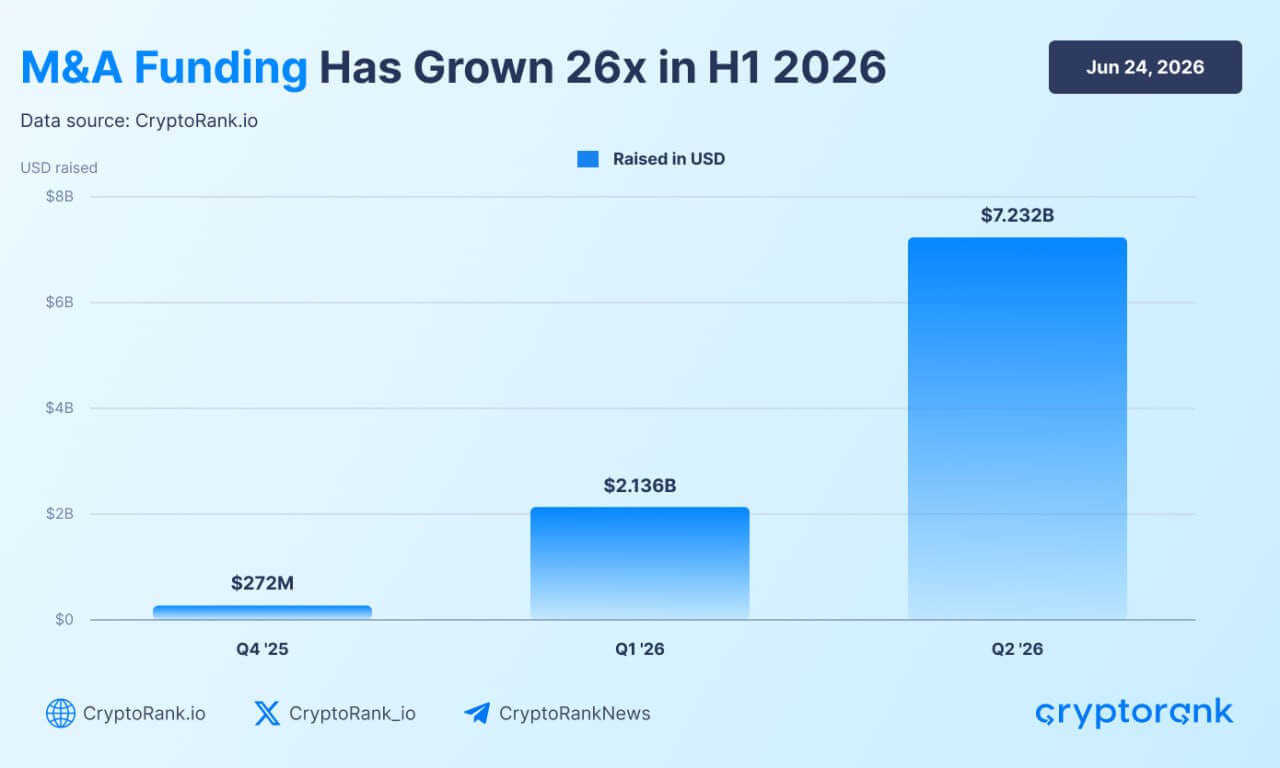

Cryptocurrency mergers and acquisitions reached $7.23 billion within the second quarter of 2026, up from $2.14 billion within the first three months of this 12 months.

Over the previous two quarters, whole capital deployed by way of transactions was $9.37 billion. CryptoRank information put the broad-based surge within the first half of the 12 months at 26x year-on-year, highlighting how buying and selling exercise accelerated quickly regardless of weakening spot market situations.

The acceleration comes as Bitcoin trades close to its lowest stage in practically two years and a few of the {industry}’s largest employers proceed to chop jobs.

This divergence reveals the place capital is shifting throughout recessions, as firms scale back spending on broad hiring and speculative development.

As a substitute, conventional monetary establishments, banks, card networks, buying and selling homes, and well-capitalized crypto companies are buying fee programs, regulatory licenses, custodian operations, and market infrastructure that may take years to construct internally.

The end result was a bear market that weakened many cryptocurrency firms with out eliminating institutional demand for the expertise.

Conventional finance fuels wave of crypto infrastructure acquisitions

Conventional monetary establishments are opting to buy totally developed digital asset infrastructure relatively than constructing compliance and expertise programs from scratch, fueling a wave of cryptocurrency acquisitions.

Banks, fee processors, and monetary expertise firms are aggressively concentrating on startups that have already got custody options, fee rails, and regulatory approvals.

This shopping for spree is essentially pushed by international coverage stabilization. The European Union’s Marketplace for Cryptoassets (MiCA) framework has established uniform licensing requirements, and ongoing stablecoin laws within the US is giving main firms the arrogance to make long-term bets.

Authorized and advisory consultants level to this coverage help as a serious catalyst. In keeping with Architect Companions’ Q1 Cryptocurrency M&A Funding Report, the banking and securities industries are totally embracing blockchain, repositioning blockchain expertise as a foundational layer of conventional monetary markets.

Mastercard’s $1.8 billion acquisition of stablecoin firm BVNK is a main instance. The acquisition enabled the cardboard community to instantly safe the expertise and licenses wanted to course of stablecoin funds, bypassing years of inner growth.

Different Wall Road heavyweights are additionally gaining strategic footing by way of focused investments. Intercontinental Trade is backed by prediction platform Polymarket, Citadel Securities, which invested in brokerage agency Alpaca, and market maker Keylock, which is backed by Normal Chartered’s enterprise arm.

Asset administration firms are additionally conducting outright acquisitions to seize demand from institutional buyers. Franklin Templeton, which manages $1.7 trillion in property, just lately launched a devoted digital asset division referred to as Franklin Crypto.

The transfer was accomplished with the acquisition of 250 Digital, which absorbed the agency’s funding crew and liquid crypto methods beforehand managed beneath CoinFund, offering actively managed cryptocurrency merchandise on to Franklin Templeton’s international consumer base.

Non-public capital typically strongly helps firms that join blockchain to the broader monetary system. Q1 funding information confirmed a transparent choice for stablecoin utilities corresponding to international change, company funds, and cross-border funds over speculative crypto-native tasks.

On this setting, regulatory credentials act as a serious aggressive moat. goal Corporations with broker-dealer capabilities, federal financial institution charters, or registered funding advisor standing, corresponding to Alpaca, Anchorage, and Superstate, appeal to stronger purchaser curiosity as a result of they supply acquirers with: Fast authorized permission to function.

Whereas conventional finance flexes its stability sheet, blockchain networks are quietly rising as a brand new class of aggressive consumers.

Traditionally, Layer 1 and Layer 2 networks relied on impartial builders to construct functions on-chain. These networks, now going through intense competitors for customers, are buying direct-to-consumer functions.

Polygon’s current acquisitions of Coinme and Sequence spotlight this axis. By buying fee entry and pockets infrastructure, blockchain has ensured a singular end-to-end consumer expertise and stuck transaction volumes, demonstrating that technical capabilities alone are now not sufficient to keep up market share.

Cryptocurrency-related job cuts will turn out to be extra critical as AI and compliance reshape the workforce

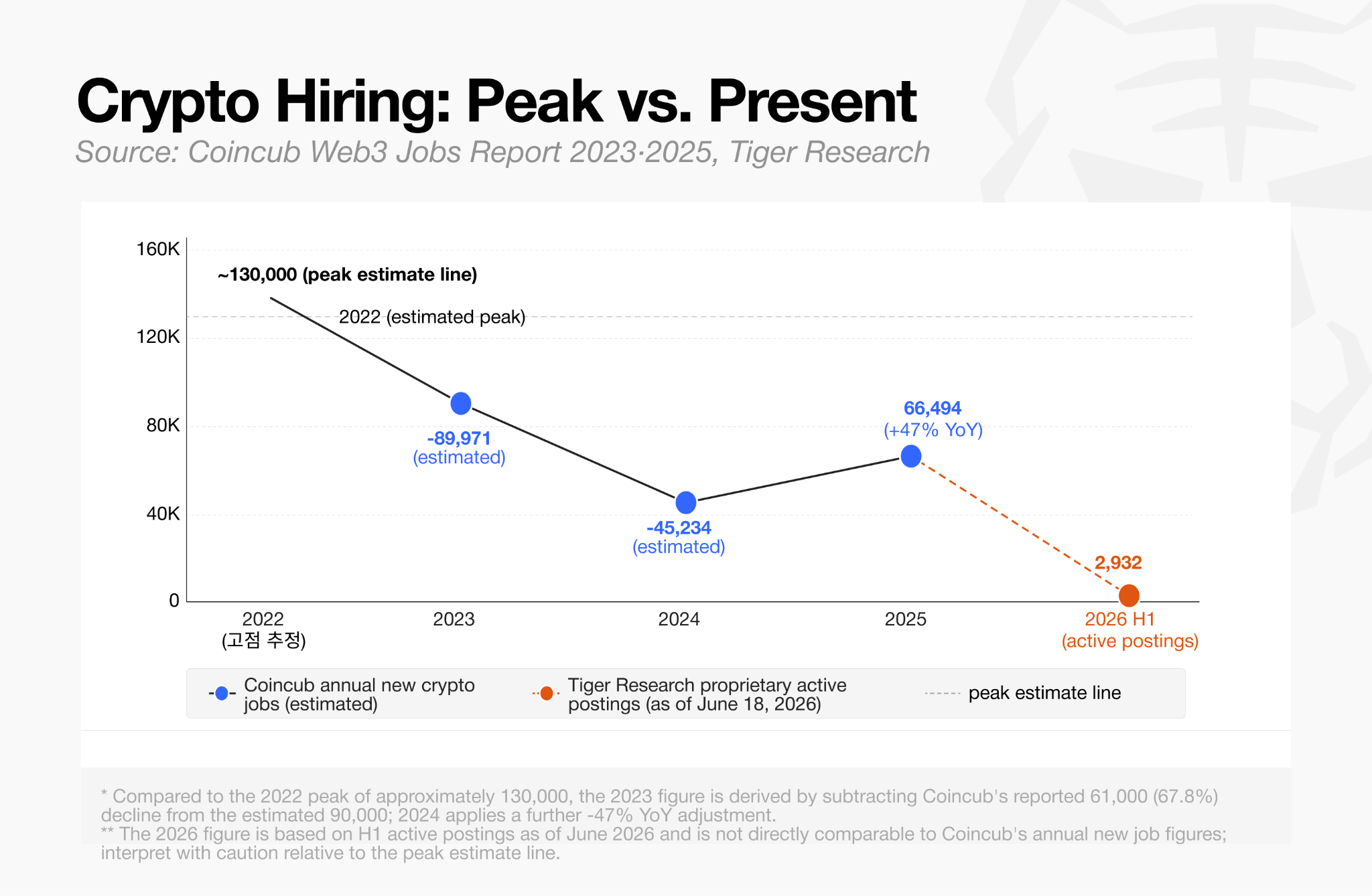

The tempo of company acquisitions stands in sharp distinction to the continued contraction of the digital asset labor market.

In keeping with June 2026 information compiled by Tiger Analysis, there are presently solely 2,932 energetic jobs on this {industry} worldwide.

This quantity is a shadow of the aggressive recruiting efforts seen in 2021 and early 2022, when buying and selling platforms, decentralized finance protocols, and NFT markets have been all increasing headcount on the similar time.

The hiring recession, which started through the 2022 market downturn and accelerated after FTX’s collapse, has seen the variety of job openings drop by about 40% throughout North America and Europe. The market has not but recovered to its earlier heights.

Actually, layoffs continued steadily by way of the primary half of this 12 months. Main platforms corresponding to Gemini, Coinbase, Kraken, Algorand, Crypto.com, and most just lately the Ethereum Basis have launched new discount rounds.

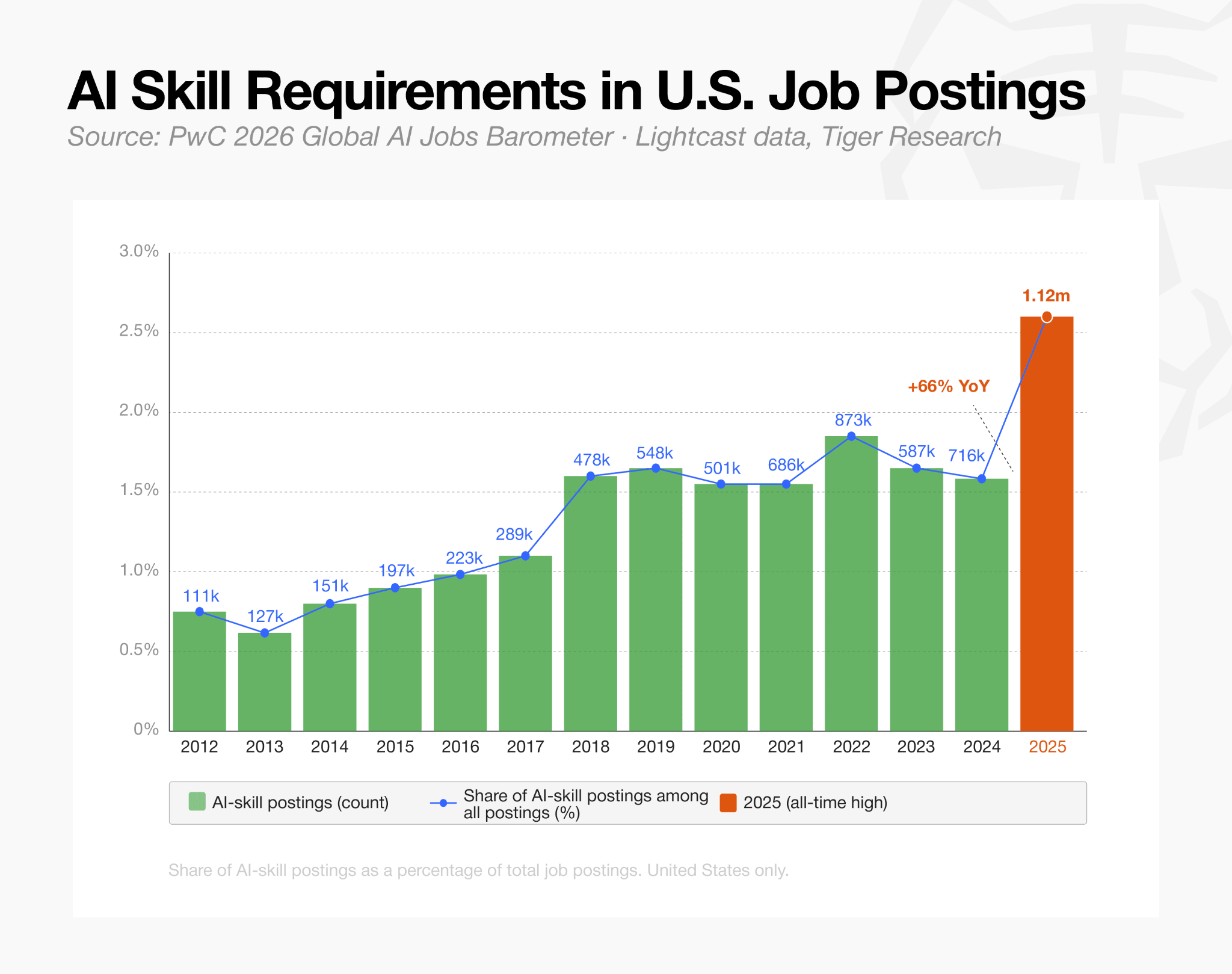

Executives cited weak token valuations, broader macroeconomic pressures, and diminished operational effectivity resulting from synthetic intelligence as elements for the downsizing. For context, Coinbase has clearly framed its restructuring as a transition to an “AI-native” working mannequin.

This technological shift can also be evident in recruitment information. The proportion of crypto job listings that require AI proficiency greater than doubled in a single 12 months, leaping from 23% in early 2025 to greater than 53% by March 2026.

Though general employment stays depressed, the composition of the workforce is essentially altering. Corporations should not implementing blanket hiring freezes. Relatively, we’re actively narrowing our focus to technical and regulatory experience.

In keeping with Tiger Analysis, roughly 34% of energetic job openings are for engineering roles, whereas authorized and compliance positions account for about 10%. This shift is extra pronounced on centralized exchanges, the place compliance-related positions account for 16% of job openings and outnumber gross sales and enterprise growth positions by greater than 2-to-1.

This reveals that these firms are prioritizing the workers wanted to safe licenses, handle threat, and preserve core infrastructure whereas decreasing spending on advertising and group development.

Moreover, the restricted adoption that does exist is extremely concentrated inside a small variety of main firms, relatively than being dispersed throughout early-stage startups. Centralized exchanges generate nearly a 3rd of all open positions.

The stablecoin and funds sector can also be a much bigger half, however its actions are fairly centralized. Tether and Ripple alone account for over 80% of the record in that class.

Finally, this information paints an image of focused company restructuring and defensiveness relatively than an industry-wide labor market resurgence.

Cryptocurrency firms in monetary bother turn out to be acquisition targets

Blockworks’ current acquisition of Messerli completely encapsulates the intersection of widespread layoffs and accelerating consolidation.

Cryptocurrency analytics agency Blockworks acquired the analytics supplier for about $10 million, a steep drop from its valuation of $300 million after a capital improve in 2022. Previous to the sale, the analysis agency had endured three separate rounds of job cuts beginning in 2023.

This deep low cost highlights the cruel actuality examine going through digital asset startups that depend on enterprise capital, promoting, or subscription fashions.

Shrinking runway and sluggish income era are forcing small and medium-sized companies to the negotiating desk, permitting well-capitalized consumers to soak up specialised expertise, proprietary information, and distribution at a fraction of earlier non-public market valuations.

Business analysts anticipate these monetary pressures to quickly spill over into the digital asset treasury sector. All through 2025, various publicly traded monetary establishments efficiently raised capital by buying and selling at a premium in comparison with their crypto reserves.

Nevertheless, resulting from a mixture of low token costs and poor inventory efficiency, many of those automobiles are price lower than their underlying holdings. This low cost considerably limits the power to challenge further shares to additional accumulate tokens.

Galaxy Digital researchers recommend {that a} enterprise mixture gives a viable path ahead for these firms. A well-positioned treasury agency like Michael Saylor Technique might purchase friends at a reduction and consolidate their stability sheets whereas concurrently concentrating on revenue-generating working companies and decreasing their reliance solely on rising token costs.

In the meantime, the M&A wave, supported by a mature authorized framework, might ultimately contain decentralized and autonomous organizations as effectively.

Current legislative developments, corresponding to Wyoming’s Unincorporated Nonprofit Affiliation (DUNA) construction, have given DAOs acknowledged authorized mechanisms to carry off-chain property and mental property.

Clearer governance and possession will make it simpler for protocol treasuries to pursue acquisitions of complementary software program tasks and devoted growth groups.

Nonetheless, these decentralized mergers stay extremely experimental in comparison with the normal compliance-driven acquisitions that dominate the present market cycle.

Capital remains to be accessible however has turn out to be selective

Cryptocurrency buying and selling exercise is approaching $10 billion within the first half of 2026, however capital allocation is changing into extra selective.

A notable exception to this strictly institutional focus is the prediction market sector. Occasion betting platforms have been vying for mainstream dominance and garnering large funding.

For context, Kalsi is reportedly negotiating a funding spherical valuing the federally regulated change at $40 billion. That is nearly double the earlier $22 billion price ticket. As competitors for prediction market supremacy intensifies, polymarkets are absorbing vital help as effectively.

However past predictions, the enterprise’s thesis has narrowed dramatically. Capital is overwhelmingly flowing into companies that bridge the hole between digital property and the normal monetary system.

Tokenization firms and institutional buying and selling homes are securing massive checks to tout sustainable, insulated income fashions that cost banks, brokerages and asset managers for regulated companies relatively than counting on the fickle retail crypto merchants. Superstate just lately closed an $82.5 million spherical to develop its blockchain-based securities issuance, giving Alpaca a dominant place in tokenized US fairness and exchange-traded fund settlement.

This funding trajectory reveals buyers are shifting their bets from conceptual tokenization trials to precise regulated monetary merchandise.

Clearly, pure decentralized finance protocols and experimental base layer blockchains have been utterly lacking from this quarter’s mega-rounds.

This selective enterprise capital deployment displays broader M&A developments. Liquidity exists, however it’s ring-fenced for startups that boast regulatory licenses, institutional distribution channels, and tangible utility to conventional finance.

The bear market has successfully pruned the {industry}, forcing weak fashions to consolidate or lay off workers, whereas closely rewarding infrastructure suppliers constructed to outlive the crypto winter.