Bitcoin’s second-quarter decline unfolded in parallel with a uncommon contraction within the stablecoin market, including one other signal that liquidity in cryptocurrencies is weakening past simply spot costs.

Bitcoin’s buying and selling worth fell beneath $60,000 throughout the quarter, its lowest stage since 2024, and fell 14% over the second quarter. On the similar time, the entire stablecoin provide decreased to $312 billion, down greater than $3 billion from the earlier quarter, CEX.IO mentioned in a report shared. crypto slate.

This decline marks the primary quarterly decline in stablecoin provide since Q3 2023. Though the decline was small in proportion phrases, it was brought on by the broader crypto market shedding 6.2% of its worth.

This elevated stablecoins’ share of whole crypto market capitalization from 13% to 14%, displaying that regardless of capital flowing out of the sector, buyers nonetheless maintain a big portion of the market in dollar-linked tokens.

Stablecoins are sometimes handled as a money layer for cryptocurrencies. Merchants use them to maneuver between exchanges, settle trades, park funds, and entry decentralized finance.

Due to this fact, a decline in provide doesn’t routinely imply customers will abandon stablecoins, however it does point out that fewer digital {dollars} are circulating available in the market as buying and selling, remittance, and speculative exercise additionally weakens.

Excessive-yield merchandise are a hindrance

Probably the most speedy modifications got here from high-yielding stablecoins, which have been one of many strongest components of the market since mid-2023.

After almost three years of quarterly will increase, the class fell by greater than $3.5 billion, or 15%, within the second quarter. This decline reversed the 19% enhance within the first quarter and demonstrated how rapidly demand shifted away from crypto-native yield methods as market situations deteriorated.

Ethena’s sUSDe accounted for many of the decline. Market capitalization fell 52%, wiping out almost $2 billion in market capitalization. Sky’s sUSDS additionally fell, dropping 16% throughout the quarter.

These two property helped gas the early progress of high-yield stablecoins, however grew to become a supply of strain as customers lowered their publicity.

Conversely, institutional buyers’ give attention to yield has shifted to merchandise backed by actual property (RWA) and short-term U.S. authorities bonds. BlackRock’s BUIDL tokenized fund rose 2%, whereas various authorities bond-backed merchandise equivalent to USYC and USDY rose 16% and 66%, respectively.

This bifurcated efficiency indicators a transparent flight to the protection of the stablecoin market itself, with capital shifting away from algorithmic and artificial DeFi mechanisms to conventional monetary devices with regulated yields.

Layer 2 community loses stablecoin steadiness

This shrinkage additionally manifested itself in all the blockchain community, notably in layer 2 of Ethereum.

The provision of stablecoins on the Ethereum scaling community fell by 24%, or $4.34 billion, within the second quarter. This was the sector’s largest quarterly decline because the fourth quarter of 2022.

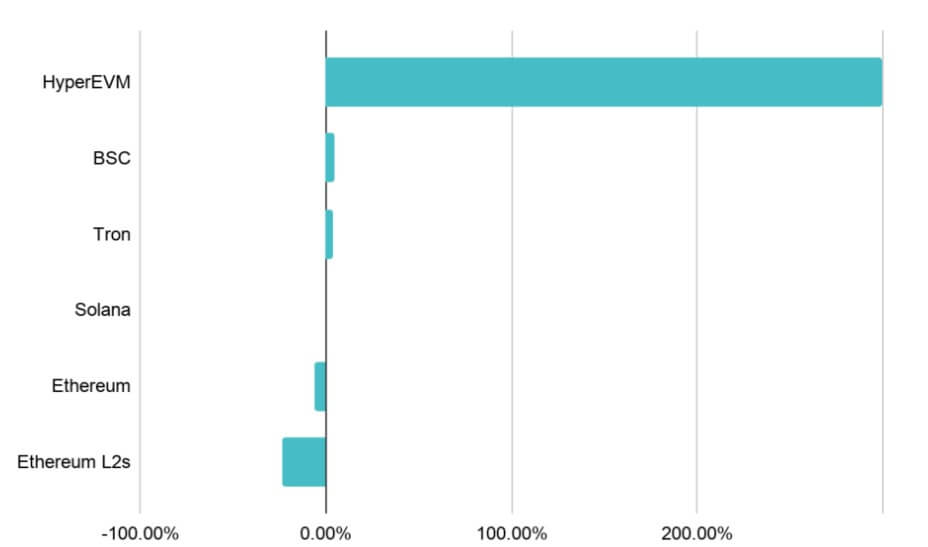

Arbitrum accounted for many of the decline. The corporate’s stablecoin provide decreased by 45%, shedding $3.5 billion throughout the quarter. This community beforehand benefited from its position as the first path to Hyperliquid.

HyperEVM’s personal stablecoin provide elevated by 300% to $5.6 billion, indicating that some liquidity moved away from Arbitrum moderately than leaving the market completely.

Ethereum’s base layer recorded a fair larger absolute decline, with greater than $10 billion in stablecoin provide misplaced. Based on CEX.IO, this was Ethereum’s steepest quarterly decline since Q1 2023.

Different networks moved in the wrong way. Tron added $3.4 billion to the stablecoin provide, and BNB Chain gained $700 million.

The rise in these chains is primarily associated to cost actions, indicating that stablecoins used for remittances and funds are extra resilient than stablecoins related to DeFi and transaction flows.

Community-level knowledge exhibits that the market shouldn’t be shrinking evenly. Whereas some crypto-native liquidity channels weakened sharply, payment-focused chains continued to develop.

This distinction may dictate how rapidly the market stabilizes if buying and selling exercise stays subdued.

USDC expands share as transactions decline

Clearer affirmation of the general slowdown appeared in community exercise metrics, however USDC stood out as an exception.

CEX.io mentioned whole stablecoin buying and selling quantity decreased by 18% to $6.8 trillion. USDT buying and selling quantity decreased by 24%, reflecting a broader decline in crypto buying and selling exercise.

In the meantime, USDC’s buying and selling quantity elevated by 34%, making it the one main stablecoin to file a rise in absolute buying and selling quantity throughout the quarter. Because of this, USDC’s share of the entire digital forex buying and selling quantity rose to 12.5%, a file excessive. The earlier excessive was 11%, recorded within the fourth quarter of 2023.

This transformation partly displays modifications in centralized overseas alternate markets, notably in Europe. Tether has not secured authorization beneath the European Union’s Marketplace for Cryptoassets (MiCA) framework, and the alternate has lowered its USDT assist at regulated amenities in Europe.

This creates extra room for USDC to learn from Circle’s compliance place within the area.

CEX.IO’s platform knowledge confirmed an analogous sample. USDC accounted for 60% of stablecoin-related monetary exercise on exchanges in Q2, up from 58% in Q1 and 27% in Q1 2025.

This quantity exhibits that USDC is on the rise regardless of a cooling general buying and selling atmosphere. It will give Circle’s tokens a stronger place in regulated alternate exercise, whereas placing USDT’s dominance beneath additional strain in a market with more and more stringent compliance necessities.

Migration exhibits widespread slowdown

Notably, the clearest signal of low exercise within the stablecoin sector comes from transaction knowledge.

The variety of stablecoin transactions within the second quarter fell to 4.48 billion, down 530 million from the earlier quarter. CEX.IO mentioned this was the most important absolute quarterly decline ever. The 11% decline was additionally the most important proportion decline since This autumn 2022.

Even after eliminating bots, automated non-economic actions, the slowdown was nonetheless noticeable. The adjusted variety of transactions decreased to 613 million, down roughly 11 million from the primary quarter.

The small lower in adjusted exercise means that many of the general lower is because of infrastructure-related and automatic flows, moderately than bizarre customers alone.

Adjusted buying and selling quantity additionally decreased. Natural stablecoin remittances decreased by 5.5% to $4.09 trillion, ending 10 consecutive quarters of progress. The 18.3% enhance within the first quarter was adopted by a reversal, with a extra pronounced decline within the second quarter.

Nonetheless, smaller transfers had been higher tolerated. Remittances of lower than $250 rose 5% to $19.39 billion. This enhance means that retail-scale funds and peer-to-peer exercise remained lively at the same time as large-scale remittances slowed.

The distinction between small and enormous transfers is necessary for the second half of the 12 months. If small-value funds proceed to extend whereas high-value transactions and infrastructure flows decline, stablecoins may develop into much less tied to crypto market cycles over time. Nevertheless, if bigger flows proceed to say no, the market may face an extended liquidity reset.

Rules reply to market downturn

The outlook for the second half of the 12 months will rely partly on whether or not rules usher in new demand quick sufficient to offset the droop in crypto-native exercise.

In Europe, the MiCA transition interval ended on July 1, forcing crypto-asset service suppliers to function beneath the bloc’s licensing regime or stop providers to EU clients.

This might proceed to reshape stablecoin buying and selling pairs, particularly if exchanges transfer away from USDT to regulated options.

In the USA, the GENIUS Act requires clearer provisioning, redemption, and oversight requirements for stablecoin issuers. The CLARITY Act may add a broader market construction framework for digital property, however its path stays tied to the Senate agenda and unresolved political battles.

Conventional monetary firms are additionally getting deeper into stablecoins. By the use of background, SoFi and MoneyGram have introduced plans for a stablecoin, and Japan’s three largest banks are creating a joint yen-pegged token.

These efforts recommend that regardless that crypto-native demand weakened within the second quarter, institutional investor curiosity stays.

The query is whether or not new funds, banking and real-world asset use instances can offset the strain from decrease buying and selling exercise.

In the course of the 2022-2023 recession, it took a few 12 months for stablecoin provide to return to sustained progress.

Nevertheless, the present cycle could not align with that timing, because the market is extra various than it was three years in the past.