The outdated Bitcoin technique ran on the straightforward logic that as international M2 expands, capital flows into dangerous property and Bitcoin positive aspects a disproportionate share.

This relationship was the driving pressure behind the 2020-2021 bull market, with crypto Twitter spending a lot of 2024 charting the M2 overlay as proof that the following leg was imminent.

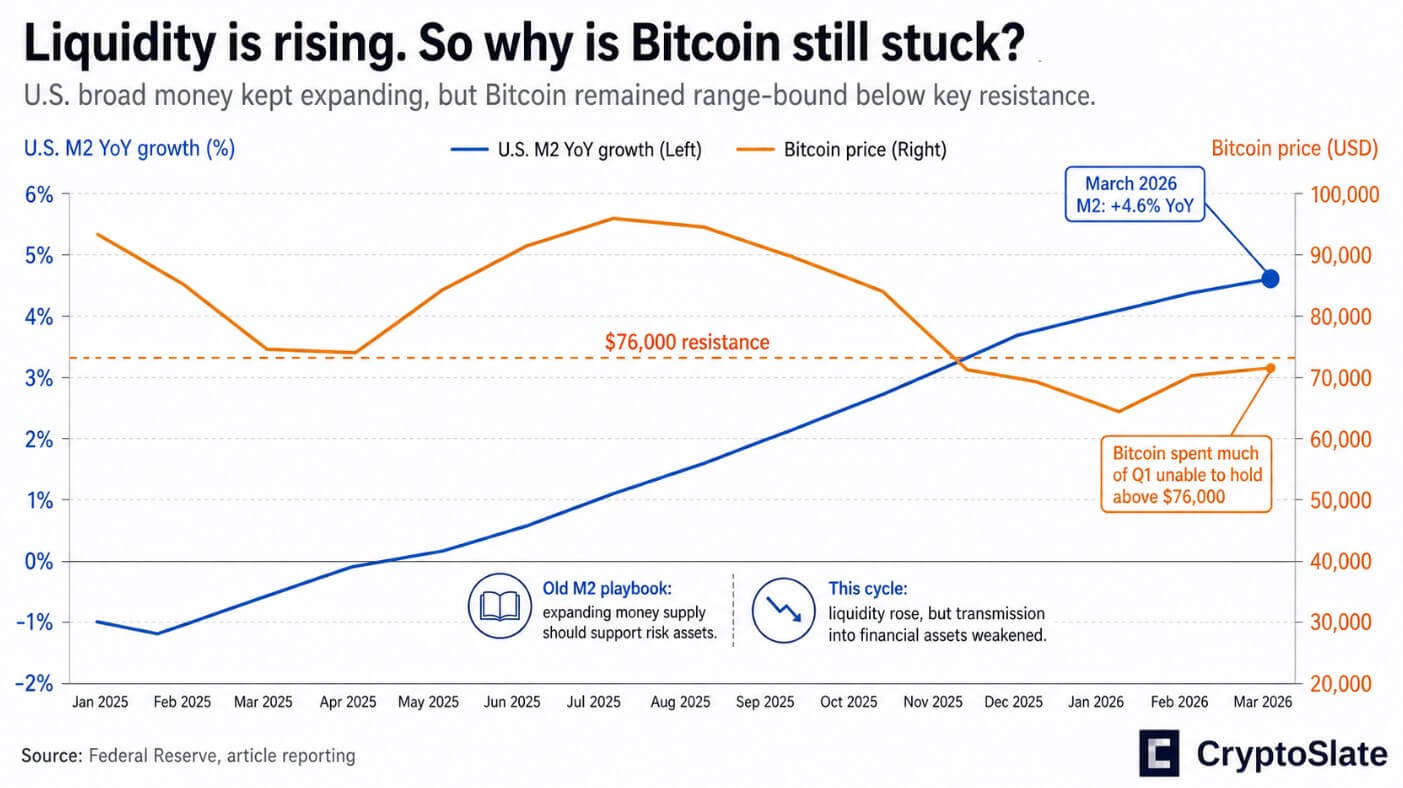

At present, international M2 is increasing, however Bitcoin continues to underperform.

U.S. M2 issuance in March 2026 was roughly $22.7 trillion, up 4.6% year-on-year, and Bitcoin spent a lot of the primary quarter failing to interrupt above $76,000, a degree that RealVision chief crypto analyst Jamie Coutts recognized as a key resistance on CryptoQuant’s Unbiased podcast.

Coutts’ analysis was that the transmission mechanism had modified, as the kind of liquidity decided whether or not the enlargement truly reached monetary property.

Since Quantitative Easing in 2008, the Federal Reserve has bought property immediately, flooding the system with financial institution reserves which have nowhere to go however shares, credit score, and ultimately cryptocurrencies.

Treasury issuance, reserve administration, money steadiness fluctuations, and financial institution credit score creation have now changed the fireplace hose of central financial institution steadiness sheets.

plumbing issues

U.S. public debt ended the fourth quarter of 2025 at greater than $38.5 trillion, up 6.3% from the identical interval final 12 months. In the meantime, US M2 grew by 4.6% over the identical interval.

Primarily based on essentially the most fundamental numbers obtainable, debt outpaces frequent cash by nearly 2 share factors annually. The excellent debt is at the moment equal to roughly 1.70 instances the full quantity of M2, an unprecedented ratio in right now’s accommodative monetary setting.

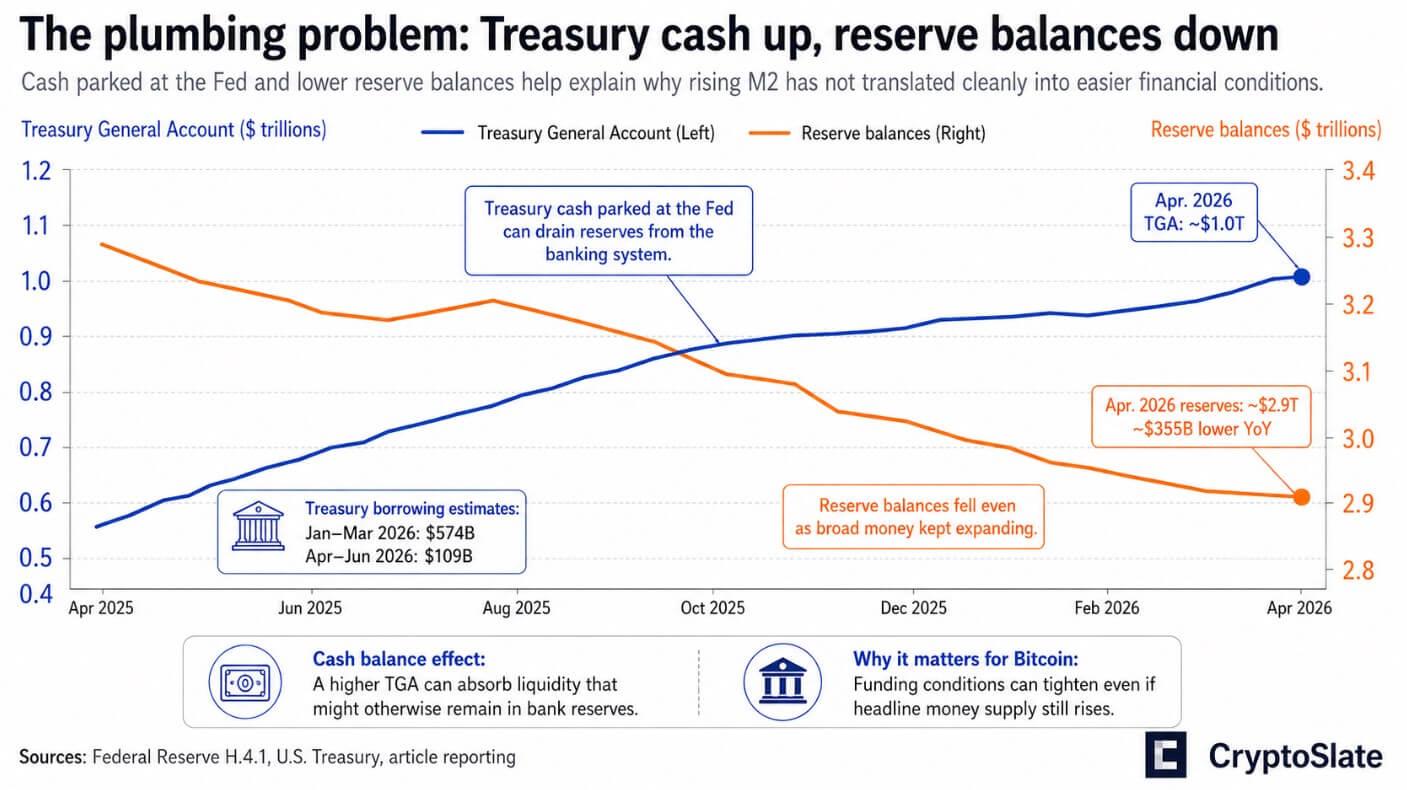

In keeping with the Ministry of Finance’s personal borrowing estimates, internet marketable debt will rise to $574 billion within the January-March interval of 2026, and an extra $109 billion within the April-June interval, with the money steadiness exceeding $1 trillion.

The Treasury Division’s Common Account, a part of the Federal Reserve Board, has roughly $1 trillion of up-to-date H.4.1 knowledge. At the same time as M2 continues to rise, money held on the Fed drains reserves from the banking system.

The Fed introduced on April 22 that its reserve steadiness had fallen to about $2.9 trillion, a lower of about $355 billion from the identical interval final 12 months.

Whereas broad cash is increasing on paper, the traces that really transfer reserves into monetary markets are straining on the final minute.

Financial institution credit score continues to be increasing, with business loans and leases reaching about $13.7 trillion by mid-April, nevertheless it seems to be being absorbed into the true economic system.

On the FOMC assembly on April 29, the coverage rate of interest remained unchanged at 3.5% to three.75%, and whole property remained at roughly $6.7 trillion. Officers cite inflation as the primary restraint, and increasing the steadiness sheet shouldn’t be on the agenda.

Why the outdated chart broke

In his podcast, Coutts argued that Bitcoin’s weak point displays friction within the plumbing.

The decline in late 2024 and early 2025 was triggered by tightening of reserve necessities within the fourth quarter, Treasury actions associated to the federal government shutdown, derivative-led deleveraging, and the rising position of ETFs and derivatives markets in Bitcoin’s worth construction.

None of those forces seem within the international M2 overlay as a result of they’re traits of the monetary system, the place Treasury provide, reserve administration, and funding circumstances are the true battlegrounds.

Gold supplies the clearest affirmation between markets. In keeping with the World Gold Council, central banks bought 244 tonnes of gold within the first quarter, a rise of three% year-on-year, bringing whole demand for gold to 1,231 tonnes and a report $193 billion in worth phrases.

Public establishments are hedging the credit score of presidency bonds on a big scale, and they’re doing so by gold, an asset that central banks can legally maintain.

The IMF’s newest fiscal monitor reveals that international public debt is on monitor to succeed in 100% of GDP by 2029, with the US and China driving a lot of the acceleration.

The Congressional Finances Workplace initiatives that the federal deficit can be $1.9 trillion in 2026, and public debt will develop from 101% to 120% of GDP by 2036, making a structural oversupply that can proceed to compete with threat urge for food for a similar pool of reserves and capital.

2 outcomes

Within the bullish case, inflation cools towards the trail the Fed expects, Treasury money balances decline, reserves are rebuilt, and financial institution credit score continues to broaden with out concern of development.

On this state of affairs, the speculation that “liquidity continues to be increasing” regains momentum. Bitcoin may very well be quickly revalued because the debt and liquidity mismatch prevents marginal monetary tightening.

Coutts handled the $60,000 zone as a price ground, predicting higher than 50-50 odds with the cycle low already in place.

Within the bearish case, debt issuance stays heavy, inflation stays excessive, Treasury funding stays tight, and the Fed can not ease the inflation it has suppressed for 2 years with out reigniting it.

Bitcoin then behaves much less like a monetary hedge and extra like a high-beta threat asset that’s uncovered to rates of interest, funding circumstances, and periodic deleveraging.

S&P International’s preliminary PMI numbers for April already clarify that development is working at a tempo near 1% per 12 months. This fragile enlargement doesn’t must fall into recession to trigger the sort of funding shock that can hit Bitcoin the toughest.

| factor | bull case | bear case |

|---|---|---|

| inflation | Cooling down for Fed’s anticipated path | Stay sticky sufficient to maintain policymakers cautious |

| Treasury money steadiness | decreases and the outflow of reserves decreases. | Keep excessive requirements and proceed absorbing liquidity |

| reserve steadiness | Rebuild from present degree | Keep agency or fall additional |

| issuance of debt | Continues to be manageable for elevated liquidity | Stays heavy and outpaces liquidity development |

| Fed’s stance | can ease or ease inflation with out reigniting it; | No significant easing is feasible with out risking one other wave of inflation |

| financial institution credit score | Proceed to broaden with out concern of development | Enlargement is weaker or offset by tighter financing circumstances |

| monetary state of affairs | loosen the clean area | Restrictive and aggravating |

| market plumbing | Treasury provide and reserves stop to behave as headwinds | Treasury funding tensions and reserve friction stay key battlegrounds |

| Bitcoin motion | As liquidity concept positive aspects momentum once more, re-rates will rise. $60,000 is held as a ground worth | Buying and selling like high-beta dangerous property with sharp drawdowns, failed breakouts, and potential for retesting decrease help |

| Key factors for traders | Elevated liquidity is adequate to soak up debt and help threat property | Liquidity should be increasing, however not quick sufficient to offset debt, reserves, and Treasury provides |

Coutts distinguishes between Bitcoin’s long-term monetary issues and the medium-term worth motion that reserve flows truly trigger.

In a regime the place debt exceeds broad funds, the Fed manages a restrictive ground, and Treasury money balances deplete reserves whilst M2 rises, a sound query for traders is whether or not the enlargement is happening quick sufficient to concurrently take in debt, reserves, and Treasury provide.

Till the debt and reserve state of affairs conclusively favors Bitcoin, the asset will proceed to expertise the sharp drawdowns and irritating consolidations that characterize a market caught between long-term constructive concept and a tougher-than-expected short-term funding setting.