In keeping with BitMEX, variations in funding charges will not be random, and understanding why they happen may give merchants a bonus.

In its newly launched Q2 2026 Derivatives Report, the trade argues that disparities in funding charges are sometimes pushed by market construction moderately than market sentiment. Components akin to collateral design, trade demographics, and index building may end up in everlasting variations in funding and recurring buying and selling alternatives.

Trying past market sentiment

Perpetual futures don’t expire like conventional futures contracts. As an alternative, exchanges make the most of fund settlements between lengthy and brief merchants to maintain perpetual costs consistent with the underlying market.

Funding charges are usually thought of an indicator of bullish or bearish sentiment. However BitMEX says that interpretation is simply a part of the story. “Whereas funding charges are sometimes seen as a easy indicator of market sentiment, the truth is far more nuanced,” he stated. peter wilkinsonCEO of BitMEX.

“Our analysis reveals that structural components akin to collateral sort, trade participant profile, and index building can create persistent funding charge variations that merchants can determine and strategically exploit.”

In keeping with the report, merchants ought to first determine: What’s inflicting the funding scarcity? earlier than trying to commerce.

Three components behind the distinction in funding charges

This report identifies three structural components that constantly influence funding charges throughout the crypto derivatives market.

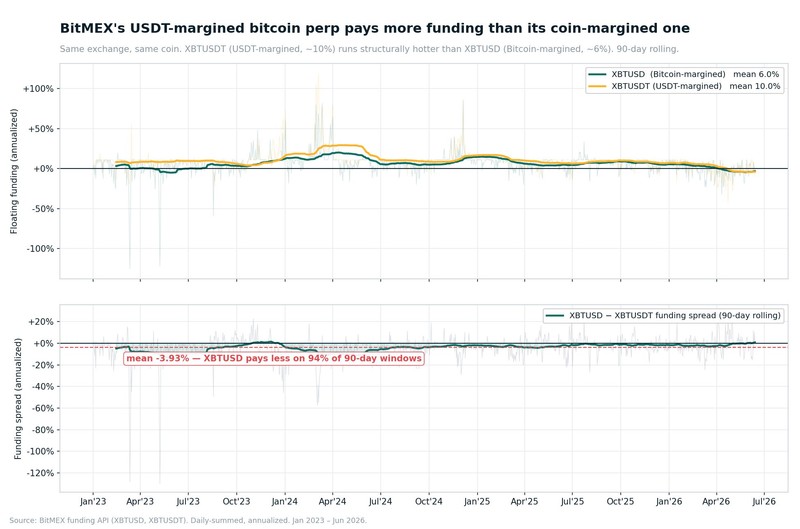

The primary one is Extra design.

BitMEX’s XBTUSD and XBTUSDT Perpetual each monitor Bitcoin, however they use completely different collateral. One is margined with Bitcoin and the opposite makes use of USDT.

Its traits entice several types of merchants and create long-term capital spreads.

On common, the distinction in funding between the 2 contracts is roughly 3.93% each year It has been adverse for the previous three and a half years. 94% 90 day rolling interval.

The second issue is trade demographics.

When evaluating main buying and selling venues, BitMEX discovered: Hyperliquid’s Bitcoin perpetuals generated a mean annual funding premium of seven.17% over Binance Between 2023 and 2026. Ether Perpetual Securities can also be Annualized premium 5.31% over the identical interval.

In keeping with BitMEX, lots of the variations replicate variations within the consumer base.

Hyperliquid’s retail-focused on-chain buying and selling setting tends to keep up larger funding charges, whereas Binance’s bigger institutional presence helps compress spreads by means of arbitrage.

The report argues that operational hurdles akin to custody necessities, compliance restrictions, and cross-chain capital actions proceed to restrict institutional investor participation in decentralized exchanges, permitting funding premiums to persist.

The third issue is Index building.

Why oil financing reached -531%

One of many report’s most spectacular findings comes from the tokenized items market.

Not like Bitcoin perpetual contracts, oil contracts can’t reference a repeatedly traded spot market. As an alternative, it derives its value from the earlier month’s futures contract.

As these futures costs transfer from one contract to the subsequent in the course of the backwardation interval, the value index will mechanically decline, even when the underlying value of oil stays unchanged.

In keeping with BitMEX, this course of will briefly cut back the funding quantity of the WTIUSDT perpetual contract to roughly Annual charge -531% April 2026 futures on roll.

The trade stated the episode reveals that funding charges may be pushed solely by trade mechanics, moderately than dealer positioning or broader market sentiment.

perceive the chance

BitMEX believes that merchants ought to perceive the structural forces that make the distinction between funding charges and never merely deal with them as market indicators.

This report explores how funding alternatives emerge throughout quite a lot of margin fashions, buying and selling venues, and perpetual merchandise, whereas encouraging merchants to tell apart between long-term structural inefficiencies and short-lived market occasions.

The conclusion is easy and clear. Funding charges alone do not inform the entire story.

Understanding why funding charges differ can show to be simply as invaluable because the funding charges themselves. The total report “3 Sources of Funding Price Alpha” is out there on the BitMEX Weblog.