Is a 2008-style international financial collapse on the horizon? And does the present state of affairs resemble the early levels of a broader international monetary disaster, pushed by debt prices, inflationary pressures, and constrained coverage responses?

These questions have gotten more and more troublesome to disregard as stress factors come collectively within the incorrect order: excessive bond yields, excessive ranges of public debt, power shocks, persistently excessive inflation, and hovering asset valuations.

The world nonetheless has the hangover of 2008, however with totally different coverage settings. Banks are higher capitalized than they have been earlier than the worldwide monetary disaster, and the Federal Reserve’s newest monetary stability efforts nonetheless level to areas of resilience for family and financial institution stability sheets.

The 2020 analogy additionally falls aside. Whereas inflation is underneath management, governments and central banks can flood the system with assist.

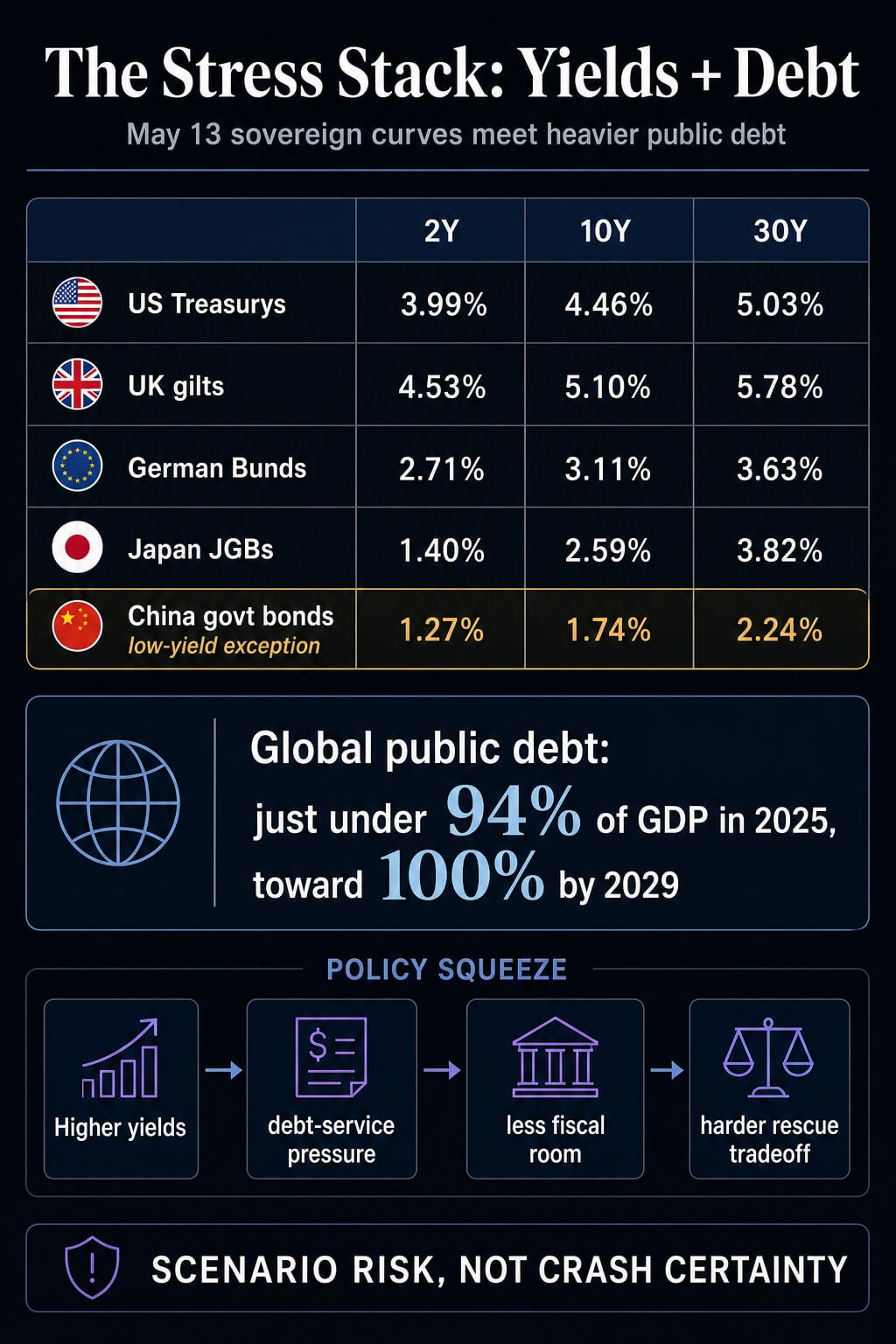

The setup is totally different as a result of the rescue trade-off is costlier. The IMF’s April Fiscal Monitor predicts that international public debt will attain just below 94% of GDP in 2025 and 100% by 2029.

The World Financial institution has warned that wars within the Center East may result in greater costs for power, meals, fertilizer and inflation. The Monetary Stability Board has marked sovereign debt markets, asset valuation and personal credit score as areas requiring shut monitoring.

The result’s a dependable and rational worst case, however the inevitability continues to be exterior the proof.

Sovereign yields return to international monetary disaster warning ranges

(Editor’s notice: Intraday volatility was very excessive in the present day, Could thirteenth. The snapshot used on this article was taken round 14:00 UTC)

The issue begins with the bond market. in the course of the day Nationwide debt knowledge As of in the present day, Could 13, the rates of interest on US Treasury bonds are roughly 3.99%, 4.46%, and 5.03% for 2-year, 10-year, and 30-year bonds, respectively.

British gold was round 4.53%, 5.10% and 5.78%. German federal bonds have been round 2.71%, 3.11% and three.63%. Japanese authorities bonds hovered round 1.40%, 2.59%, and three.82%.

Historic comparisons are necessary right here. The Nasdaq had beforehand hit its highest stage since 2007, when the yield on two-year U.S. Treasuries hit 4%.

UK two-year bond yields are at their highest stage since June 2008, whereas UK 10-year bond yields are nearing 18-year highs and 30-year bond yields are nearing ranges related to 1998.

German 10-year Bunds are nearing their highest stage since Could 2011 in the course of the euro zone debt disaster. Japan’s 10-year bond yield is at a stage final seen in 1997, and the 2-year bond yield is at a stage final seen in 1995.

China is an exception. In line with Buying and selling Economics, as of Could 13, the yield on 10-year authorities bonds was about 1.74%, the yield on 2-year bonds was round 1.27%, and the yield on 30-year bonds was round 2.24%.

The curves present totally different progress and worth contexts, dividing the story into high-yield stress in developed markets and low-yield progress stress in China.

Developed nations nonetheless have greater fiscal issues. The OECD’s 2026 Debt Survey exhibits important authorities borrowing and refinancing wants throughout member nations.

Rising yields have an effect on bids, coupon prices, and political selections over time. The longer long-term rates of interest stay elevated, the extra the market will drive governments to decide on between elevating rates of interest, decreasing spending flexibility, and growing price range deficits.

In 2008, we contributed to stabilizing the monetary system by means of aggressive monetary rescue and stability sheet assist. In 2020, fiscal and financial enlargement bridged the sudden collapse in exercise.

In 2026, the debt stability will additional broaden, long-term rates of interest will rise, inflation dangers will develop into obvious, and power shocks are already included within the knowledge.

Holmes turns oil danger into coverage danger

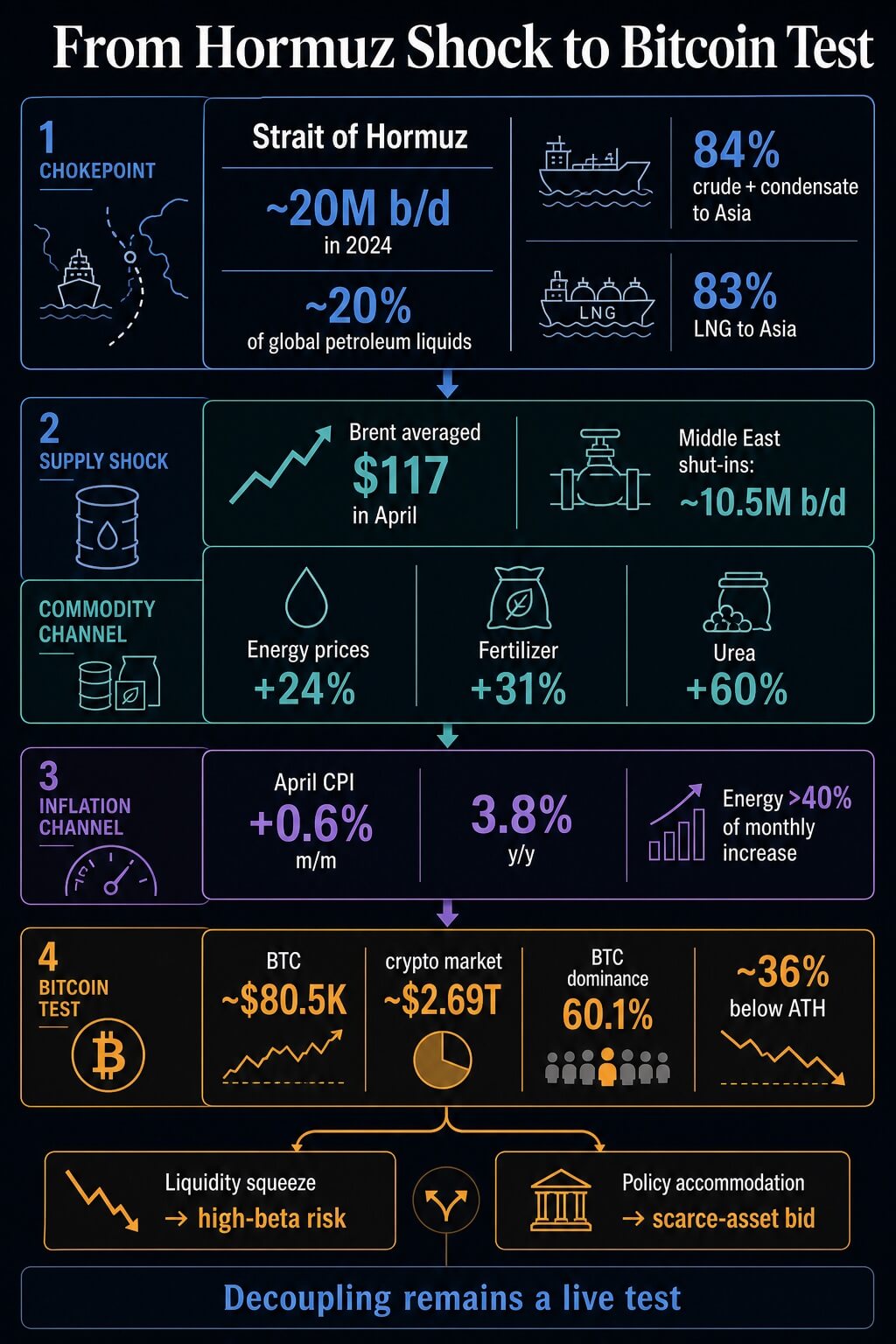

The Strait of Hormuz has develop into a serious stress level, turning regional conflicts into international price shocks. The U.S. Power Data Administration estimates that about 20 million barrels per day handed by means of the strait in 2024, representing about 20% of the world’s consumption of petroleum liquids.

The company additionally estimated that in the identical yr, 84% of crude oil and condensate and 83% of LNG through Hormuz went to Asian markets.

The present shock can also be impacting official worth and provide forecasts. In its short-term power outlook for Could 2026, EIA mentioned Holmes was successfully shut down, with Brent crude averaging $117 per barrel in April, valuing Center East manufacturing disruptions for the month at about 10.5 million barrels per day.

The company assumes that flows will start to renew in late Could or early June, however that assumption itself is an actual danger variable.

The World Financial institution’s April Commodity Market Outlook clearly describes the macro channel. Power costs are anticipated to rise 24% this yr, with Brent costs anticipated to be at $86 per barrel at baseline, with Brent costs probably rising to $115 per barrel in a extreme disruption state of affairs.

Fertilizer costs are anticipated to rise by 31% on account of a 60% hike in urea costs. The report warns that rising commodity costs will push up inflation and gradual progress, particularly in creating nations the place fiscal buffers are already restricted.

U.S. knowledge already exhibits a few of that pass-through. In line with the Bureau of Labor Statistics, the CPI rose 0.6% in April on a seasonally adjusted month-to-month foundation, and rose 3.8% year-over-year on a seasonally adjusted foundation.

Power accounted for greater than 40% of the month-to-month enhance.

That’s the mechanism that offers credibility to the crash query. Even when the shock is short-lived, inflation expectations may stay robust sufficient to delay price cuts as debt servicing prices proceed to rise.

On the similar time, weakening progress makes the coverage alternative between defending inflation credibility and monetary stability uglier.

| set off | transmission path | Destruction valve |

|---|---|---|

| Bettering sovereign yields | Authorities refinancing raises debt service prices | Debt maturities unfold the affect over time |

| holmes confusion | Oil, LNG, fertilizer and transportation prices drive inflation | Rerouting, adjusting demand and resuming transport can cushion the preliminary shock. |

| sticky inflation | Central banks have little room to intervene in market stress | Slower progress could necessitate additional changes |

| Excessive valuation and leverage | Danger property have little margin for dangerous information. | Financial institution and family stability sheets stay resilient |

| Bitcoin decoupling take a look at | BTC trades as scarce collateral or excessive beta danger | The current divergence is simply too early and nonetheless must be confirmed. |

The explanation why market assist for coverage has decreased in comparison with earlier than the worldwide monetary disaster

The stress with fairness markets is that danger property could seem calm whilst bond markets are rallying once more on the again of coverage. The Fed’s Could Monetary Stability Report mentioned the ahead price-earnings ratio remained on the higher finish of its historic distribution.

Company bond spreads remained low by long-term requirements. Hedge fund leverage remained close to document highs and was concentrated among the many largest funds.

The mixture is a matter of cushioning. In line with the identical Fed report, market contributors most frequently cited geopolitical dangers, oil shocks, personal credit score, and protracted inflation as notable dangers to monetary stability.

The FSB made an analogous level in April, saying that the battle within the Center East had already prompted a big international financial shock, with market reactions mirrored in power costs and authorities bond yields.

Meaning traders have to be cautious of conflicts throughout coverage conferences, bidding, and liquidity situations. Markets can take in excessive rates of interest when progress is robust, inflation is low, and monetary financing seems manageable.

If the central financial institution can detect worth hikes, it may possibly take in oil shocks. If borrowing prices are saved down, giant quantities of public debt will be absorbed. The present settings weaken every cushion at a time.

If the sequence is tense, a crash will naturally be the worst case state of affairs. Power and fertilizer costs stay excessive in Hormuz. Inflation stays persistent. Central banks delay assist. Lengthy-term yields stay excessive. Stress to repay debt will increase. Danger property have been priced in for a mushy touchdown on account of slowing progress and tightening liquidity.

A gentler path can also be attainable. If oil flows normalize, inflation eases, actual yields fall, and central banks pivot to supporting progress, the stress stack will probably be resolved earlier than it turns into systemic. That framework is conditional vulnerability.

This distinction is necessary for market timing. Sovereign stress tends to extend by means of bidding, refinancing calendars, credit score spreads, capital multiples, and central financial institution choices. It not often proclaims itself by means of one clear set off.

This provides the market time to adapt, but in addition means pressures could proceed to construct up even after the preliminary oil worth spike subsides. Delicate touchdown trades can overcome one shock. A harder take a look at is whether or not a number of channels can survive without delay, with every channel limiting coverage solutions to the following channel.

Bitcoin faces macro take a look at amid issues of worldwide monetary disaster

Bitcoin is a part of the macro learn, so it’s on the finish of this chain.

Bitcoin was buying and selling at round $80,500 on Could thirteenth, however whereas the new PPI pushed it beneath $80,000, the broader crypto market was round $2.69 trillion, with BTC’s dominance remaining round 60.1%.

Due to this fact, whereas it nonetheless maintains a enough dimension as a macro asset, its volatility has eliminated it from clear shelter standing.

current crypto slate The report notes that there was a time when Bitcoin behaved in a different way than U.S. shares amid stress on oil, yields and the greenback on shares. Separate evaluation from trendingcoinz frames the Holmes Shock as a watershed for Bitcoin, both a liquidity squeeze that pulls BTC again into high-beta collateral conduct or a coverage easing path that brings again scarce asset buying and selling.

That is the sober approach to deal with Bitcoin right here. Bitcoin’s monitor document as a steady inflation hedge stays unproven. The separation from danger urge for food stays incomplete.

Glassnode’s newest market developments affirm the warning. Structural enhancements nonetheless require affirmation amid macro pressures from rates of interest, oil and liquidity.

One dangerous inventory market commerce means little. The take a look at will probably be whether or not Bitcoin can maintain up if shares unload, yields stay excessive and greenback corporations and central banks are hesitant to ease inflation as it’s nonetheless supported by power and meals prices.

If BTC sustains such an setting, the narrative of economic instability will develop into even stronger. If it fails, the market will deal with it as one other dangerous asset with higher branding.

This leaves the crash query with a working reply. A repeat of 2008 continues to be out of the realm of chance, and the argument of inevitability is simply too robust.

Nonetheless, the present regime is extra fragile as a result of public debt burdens are heavier, inflation shocks are extra actual, and coverage responses are extra constrained.

A single worth chart solely tells a part of the story. Coverage selections will ship a bigger sign. If oil prices and debt servicing prices proceed to rise and central banks prioritize reining in inflation, monetary markets will face additional stress with out reduction.

If Bitcoin shifts in the direction of monetary stability, it’s going to face the clearest problem as a hedge in opposition to coverage easing and foreign money credit score danger.

In any case, the problem has moved from vigilance to danger administration. What can pull us again from the brink is that some launch valves nonetheless exist.

- Shock is conditional. As soon as the Hormuz River resumes stream and oil normalizes, inflationary impulses will subside.

- Debt stress manifests itself over time. A refinance calendar staggers the blows somewhat than forcing a single chapter.

- Our stability sheet is stronger than it was in 2008. The article cites the resilience of banks and households as limiting direct contagion, akin to the worldwide monetary disaster.

- Central banks nonetheless have freedom of alternative. These are constrained by inflation, however slowing progress or market stress may drive subsequent easing.

- There are warning indicators available in the market. It is advisable to monitor auctions, long-term rates of interest, credit score spreads, liquidity, fairness multiples, and BTC developments.